International Financial Entities Licenses in Puerto Rico

An International Financial Entities licensed in Puerto Rico under Act 273 is one of the most powerful international banking and financial services structures available. As the rules continue to tighten around offshore transactions, offshore tax benefits are reduced under President Trump, and the US increases FATCA and other regulations, expect more financial services companies to move to an International Financial Entities license in Puerto Rico.

This International Financial Entities in Puerto Rico can offer all manner of international banking, brokerage, investment management, and financial services from Puerto Rico to clients outside of Puerto Rico. Below I will detail all of the services which may be provided by this structure.

In order to qualify as an IFE in Puerto Rico under Act 273, you must hire 4 employees on the island (I usually advise clients hire 5). Then you set up an office, submit a very detailed business plan to the banking regulator, and negotiate the terms of your license.

Once approved, you will be eligible for a 20 year tax holiday on all income earned by your International Financial Entity in Puerto Rico. You will pay a 4% tax rate on all corporate profits earned by the business.

That is to say, the corporate tax rate on Puerto Rico sourced income in your IFE will be 4%.

You will also get full property and municipal licenses tax exemptions and a 6% income tax rate on distributions to PR residents. Dividends to non-PR residents will be tax free. Likewise, dividends paid to residents of Puerto Rico who qualify under Act 22 are tax free to the IFE and to the receiving party.

An IFE in Puerto Rico must be capitalized with a minimum of $550,000. Of this, $300,000 is placed on deposit with a local bank as a surety. The balance of $250,000 is your minimum corporate capital. Total authorized shares of your International Financial Entities in Puerto Rico must be $5 million (but only $250,000 of this is paid-in).

The largest firms structured under Act 273 as a International Financial Entities in Puerto Rico are international banks. For an article on this topic, see: Lowest Cost Offshore Bank License is Puerto Rico

The IFE license not limited to international banks. Family offices, insurance companies, investment advisors, hedge fund operators, currency traders, and others all operate under Act 273 as an International Financial Entities in Puerto Rico. For this reason, Act 273 is the most powerful financial services license available today.

Here’s a list of the services an Act 273 International Financial Entity licensed in Puerto Rico can offer:

- Accept deposits, including demand deposits and interbank deposits (or otherwise borrow from banks outside of PR and other IFEs)

- Place deposits with banks outside of PR and other IFEs.

- Make, procure, place, guarantee, syndicate, or service loans.

- Issue, confirm, give notice, negotiate or refinance letters of credit provided both the client and the beneficiary requesting the letter of credit are not residents of Puerto Rico.

- Discount, rediscount, deal or otherwise trade in money orders, bills of exchange, and similar instruments, provided that neither side of the transaction is a resident of Puerto Rico.

- Engage in any banking transaction permitted by Act 273 in the currency of any country, or in gold or silver, and participate in foreign currency trades.

- Underwrite, distribute, and otherwise trade in securities, notes, debt instruments, drafts and bills of exchange issued by a firm outside of Puerto Rico and purchased by a client of the IFE who is not a PR resident.

- Engage in any activity of a financial nature outside of Puerto Rico which would be permissible for a bank licensed in the United States.

- If the International Financial Entity licensed in Puerto Rico gets an additional license, it may act as a fiduciary, executor, administrator, registrar of stocks and bonds, property custodian, assignee, trustee, attorney-in-fact, agent, or in any other fiduciary capacity.

- Acquire and lease personal property.

- Buy and sell securities outside of Puerto Rico.

- Provide investment advice to persons outside of Puerto Rico.

- Act as a clearinghouse in relation to financial contracts or instruments of persons who are not residents of Puerto Rico.

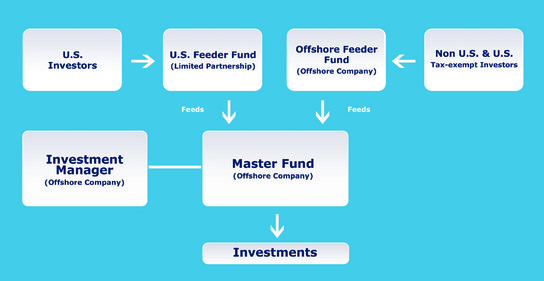

- Organize, manage, and provide management services to international financial entities such as investment companies and mutual funds. This is the section of the law used by hedge funds to manage master / feeder structures set up in Cayman with feeders in the US and Cayman.

- Dedicate itself to provide the following Services:

- Asset management,

- Management of activities related to the investment of private capital,

- Management of hedge funds and high-risk funds,

- Management of pools of capital,

- Administration of trusts utilized for converting different types of assets into securities (such as REITs),

- Management of Escrowed fund for persons who are not residents of Puerto Rico.

- Engage in any other activities approved by the Commissioner.

- With the Commissioner’s prior approval, establish branches outside of Puerto Rico. This includes the United States and foreign countries.

Section 15 above is commonly used by family offices. The clause “dedicated to” means you may only engage in these activities and will thereby be subject to reduced compliance.

For more on operating an investment fund from Puerto Rico, see: How to operate an investment fund tax free from Puerto Rico

Note that an International Financial Entities in Puerto Rico is prohibited from doing business with persons or businesses in Puerto Rico. Therefore, all of the above are limited to persons outside of Puerto Rico. An Act 273 IFE can do business with Puerto Rico’s Development Bank and its Economic Development Bank.

I hope you’ve found this article on the International Financial Entities of Puerto Rico licensed under Act 273 to be helpful. For more information on setting up an IFE in Puerto Rico, please contact me at info@premieroffshore.com or call us at (619) 483-1708.

You might also find my articles Puerto Rico’s Act 20 to be helpful, as well as a comparison between offshore tax planning and Act 20.

For more on Puerto Rico’s Act 273 vs a traditional offshore banking license, see: Top 5 Offshore Bank License Jurisdictions for 2017. For my post on the offshore FinTech, see: Offshore FinTech Bank License.

For more of my articles on the offshore bank licensing and operations, see:

- Top 5 Offshore Bank Licenses for 2017

- Lowest Cost Offshore Bank License is Puerto Rico

- Offshore Bank Advertising Rules (a review of Reg. S)

- Offshore Banking Licenses (on lowtax.net)

- Capital Reserve Requirements (on lowtax.net)

- Correspondent Accounts for Offshore Banks (on escapeartist.com)

- Best Offshore Banking Jurisdictions