International Money Lending License

The international money lending license came into its own in 2010 when the US began pushing out payday and other lenders of last resort. A number of offshore jurisdictions welcomed them with open arms and the battle with American regulators was on.

By 2012, many of these lenders moved from offshore licenses to those issued by US Indian tribes. For example, Integrity Payday Loans got in trouble with a few US states operating as a Nevis company. They became “ a tribal lending entity wholly owned by the Flandreau Santee Sioux Tribe, a federally recognized Indian tribe that operates and makes loans within the Tribe’s reservation. All loans are subject exclusively to the laws and jurisdiction of the Flandreau Santee Sioux Tribe.”

With high risk lenders fleeing for greener pastures, offshore lending, like offshore banking post FATCA, has gone mainstream. These licenses are now used by everyone from multinationals to green energy companies, such as solar loan and lease providers to fund operations and manage their worldwide tax obligations. Where payday lenders were looking to hide, the new trend is towards those looking to operate more efficiently, make use of their offshore retained earnings, bring in foreign investors, and comply with US tax reporting obligations.

Offshore Licensing Options

There are only a few ways to accomplish these goals. You can form an international bank, a captive bank, a Panama financial services company, or operate under an international money lending license.

A international money lending license is also an alternative to a fulling licensed bank. An offshore banking license is a major undertaking requiring significant capital and backend compliance. A Panama financial services company has it’s uses, but it may not offer loans. An offshore lending license is the most efficient option for a company looking to make loans within a group of companies, or to the general public (excluding residents of its issuing country), but not offer other traditional banking services (deposit taking, investments, etc.)

A money lender can be setup in a matters of weeks and at a fraction of the cost of an offshore bank. Also, corporate capital, costs of operation, and government oversight are significantly reduced.

- For more information on a fully licensed bank, see my 2015 post: Best Offshore Banking License Jurisdictions.

There are several countries offering international money lending licenses. I will focus Belize below, but a proper analysis of your needs, number of investors, number and size of your loans, and your business model, should be undertaken before selecting a jurisdiction.

Belize International Money Lending License

Licenses available in Belize include:

- International money lending license

- Money brokering services

- Money transmission services

- Money exchange services

- Mutual and hedge funds

- International insurance services

- Brokerage, consultancy, and advisory services

- Foreign exchange services

- Payment processing services

- International safe custody services

- International banking license

- Captive banking license

- General banking license

For a list of applicable legislation, see: International Financial Services Commission, Belize

A company operating under an international lending license in Belize may lend up to $5,000 per transaction and was originally written by politicians for payday lenders. Loans by an international money lender must have an initial repayment period of less than one year and shall not be secured by title to real property, a motor vehicle, tangible personal property, or any other type of collateral other than the Loan Agreement and ACH authorization agreement. Also, loans made under this license shall be made to consumers for household purposes and personal expenses only (and not for commercial purposes).

In other words, you may offer short term unsecured loans of less than $5,000 to individuals, but not businesses.

A Belize international money lending license require capital of $50,000. This amount may be increased by the IFSC depending on your business model and history. Capital reserve ratios and applicable discounts apply. The application process runs about 3 months. A complete business plan with financial projections and a proven track record in your market niche are required.

A Belize money brokering license might be a workaround to the maximum amount and term of the international money lending license. If the money being lent is coming from shareholders / partners in the business, rather than outside investors, Belize might allow you to broker the loans from your partners to your clients.

I say “might” because there are no businesses currently operating in this manner under the money brokering license. In fact, there is only one license currently active in Belize. I suggest such an application should be from a more “traditional” business, such as solar panel loans, rather than a higher risk category like payday advances.

Another, more common use of the money brokering license is to broker loans from Belize banks to your clients, earning a commission on each.

Other Offshore Licensing Jurisdictions

Another alternative to the Belize international money lending license is the British Virgin Islands Financing and Money Services License. This allows you to conduct any size lending business with persons resident in BVI and abroad. There is no maximum loan amount in the BVI statute.

For more information, see: British Virgin Islands Financing and Money Services License

Note that any regulated lending business will need to follow strict capital reserve and ratio requirements. Audited financial statements are due annually, and some jurisdictions require quarterly reporting.

The above describes international lending licenses. I suggest that the best license for an offshore leasing company is the Panama Financial Services License, which I will cover in another post.

Raising Money for an Offshore Lending Business

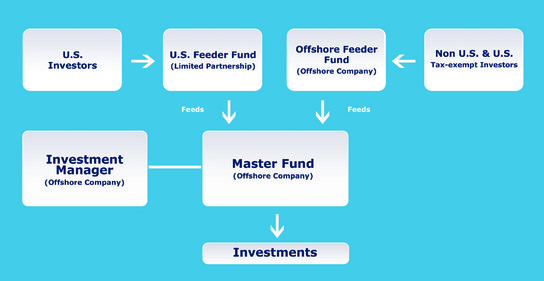

If you wish to raise capital for your offshore lending business, you will need a master-feeder offshore fund or similar structure. This is because your lending license does not allow you to take deposits from people other than partners in the business. Nor does it allow you to solicit investors.

With an offshore master-feeder fund, accredited or super accredited investors (as defined by the US SEC) may invest in your US entity and non-US persons and US tax exempt investors (IRAs, etc.) may invest in your foreign entity. Both of these feed into the master fund, which in turn invests in to your offshore lending company.

By linking a master-feeder fund to an international lending license, you can raise unlimited amounts of capital while minimizing compliance costs and regulatory oversight. You might find it advantageous to operate a fund in a jurisdiction separate from the lending company. For example, the fund could be in Cayman or Belize with the lender domiciled in BVI.

Raising capital through a fund allows you to earn a commission on the appreciation in the fund and from the primary lending business. Typical master-feeder funds earn 2% of the money under management and 20% of the appreciation after a hurdle rate ( LIBOR+2 or some similar published rate).

Conclusion

In 2015, the world of offshore licensed entities is as complex as it is diverse. Careful consideration of the available licenses and your business model must be undertaken before selecting a jurisdiction. Each country and license type is intended for a specific use and capital ratios and regulations vary widely.

Add to this FATCA, IRS reporting, tax compliance, SEC issues, and anti-money laundering statutes, and you will find that going offshore with a licensed lending company requires the support of a professional experienced in both US and international regulations.

I hope this article has beens helpful. For more information on an international money lending license, an international banking license, or an offshore master-feeder fund, please phone me at (619) 483-1708 or email Christian Reeves at info@premieroffshore.com.