Offshore Trusts and Community Property Law

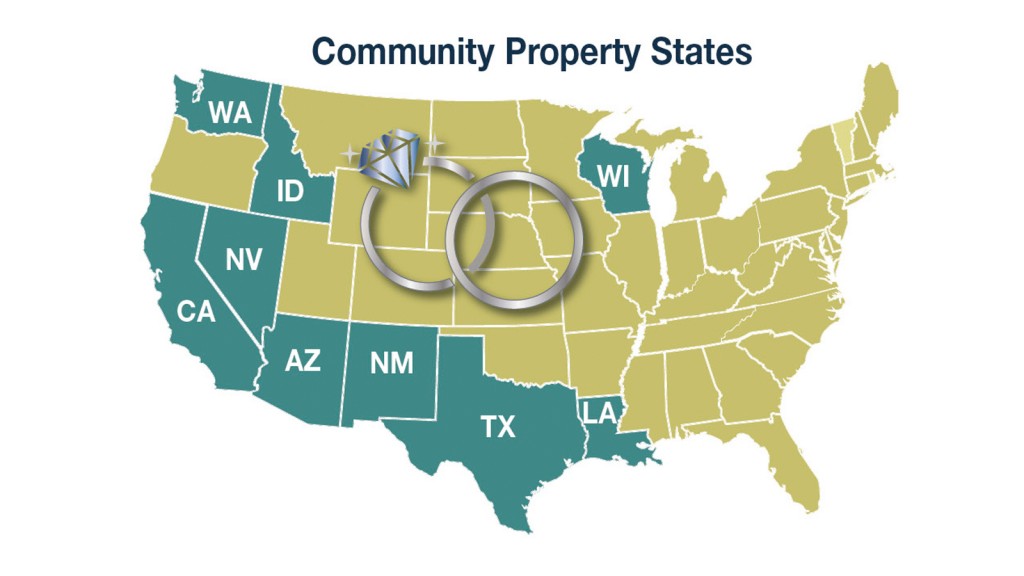

Here’s an overview of offshore trusts and community property law. If you’re married, and live in a community property state, you and your spouse must work together to form the most efficient asset protection structure. An offshore trust must include special provisions for those in community property states.

Let me frame the issue surrounding offshore trusts and community property a bit…

In a community property state, all assets are equally and jointly owned by both spouses. When one spouse passes, 100% of the assets get a step up in basis to their value at the time of his or her death.

For example, let’s say you have assets worth $1 million. You purchased them years ago for about $400,000. Thus, if you sell them, you’ll pay capital gains tax on the $600,000 profit.

When a spouse dies in a community property state, 100% of the joint property transfers to the surviving spouse. Also, the basis of that property is bumped up to the value on the date of death.

So, in the example above, the basis of the property increases from $400,000 to $1 million. If the surviving spouse were to sell all of the assets on that date, she would pay zero in capital gains tax. If the survivor holds the assets for 3 years, and they increase in value to $1.1 million, she will pay capital gains tax on only $100,000.

If this same couple didn’t live in a community property state, the surviving spouse would receive a 50% step up in basis, rather than 100%. This is because common law states view ownership as 50/50, rather than 100% by the community.

The surviving spouse would get a step up of 50%, from $400,000 to $700,000. If she sold the assets on the date of death, she would pay capital gains tax on $300,000.

Here’s how community property law impacts an offshore asset protection trust…

Most offshore asset protection trusts are structured to make transfers to them as incomplete gifts, so that the gift tax rules do not apply. When an incomplete gift is made to an offshore trust, the value of trust assets remain in your U.S. estate for federal estate tax purposes.

Because offshore trusts with U.S. settlors / owners are considered grantor trusts under the U.S. code, community property and other rules also apply. This means that, when one spouse in a community property state passes, the survivor should receive a step up in basis of 100% of the assets in the trust. If the couple lives in a common law state, 50% of the assets in the asset protection trust receive this basis increase.

The issue is that offshore trust are, by definition, formed in a foreign country. Some jurisdictions have community property statutes built in to their laws and some do not. If the country where you form an asset protection trust does not have a community property statute, the surviving spouse may not be entitled to a 100% step up in basis. In some cases she will receive only a 50% increase because the offshore jurisdiction will be considered a common law county.

For example, in California, community property transferred to an irrevocable trust loses its community property character. A poorly planned offshore asset protection trust might convert community property assets into common law assets, thereby costing you hundreds of thousands or even millions of dollars at tax time.

For this, and many other reasons, you should always hire a U.S. expert to quarterback your offshore trust.

When selecting a jurisdiction for an offshore trust for a community property client, we often start with the Cook Islands. This country was the originator of the offshore asset protection trust and is always working to improve it’s effectiveness as a tax and asset protection tool for U.S. persons.

The Cook Islands has enacted legislation to preserve the community property character of assets and the 100% step up in basis. Section 13J of the International Trusts Act provides that where a husband and wife transfer community property into an international trust or to a trust that, subsequently becomes an offshore trust (under Cook Islands law), that property will retain its community property status. Specifically, the Cook Islands will deal with the property according to the law of the jurisdiction from where it came (the community property state).

It’s also possible to use this same Cook Islands statute to preserve the separate property status of assets held before marriage in a community property state. For example, a trust set up before marriage might include language ensuring it remains separate property. Also, if both spouses agree after marriage to separate their property with a transmutation agreement, a Cook Islands trust can be designed to enforce that agreement.

The bottom line is that, so long as both spouses agree on how to handle the assets, a Cook Islands trust can be drafted to meet their needs. It’s not possible to transfer community property into an offshore trust without both spouses consent. To do that would result in a fraudulent conveyance.

I hope you’ve found this article on offshore trusts and community property law to be helpful. Please contact me anytime for assistance in forming an offshore trust or asset protection structure. You can reach me directly at info@premieroffshore.com or call us at (619) 483-1708. All consultations are private and confidential.

Leave a Reply

Want to join the discussion?Feel free to contribute!